Comprehensive Guide to Loan Amortization: Types, Processes, and Strategies

This comprehensive guide explores loan amortization in detail, covering its definition, process, types of loans, and how borrowers can effectively manage repayments. By understanding amortization schedules and strategies, individuals can make smarter financial decisions, whether they are dealing with mortgages, personal loans, or auto financing. The article emphasizes practical steps for creating schedules and highlights the benefits of understanding this key financial concept to reduce interest costs and pay off loans efficiently.

Understanding Loan Amortization: An In-Depth Perspective

Loan amortization is a fundamental financial concept that describes the systematic process of paying off a loan through a series of fixed, scheduled payments over a predetermined period. This process ensures that the borrower gradually reduces the debt, while the lender receives interest income during the repayment cycle. Although the total monthly payment remains consistent, the composition of each installment shifts over time—initial payments predominantly cover interest, with more towards principal repayment as the loan matures. This approach promotes predictable payments, easing financial planning for borrowers.

Beyond loans, amortization also finds its place in accounting, where it refers to allocating the cost of an intangible asset over its useful life. This method ensures accurate financial reporting and tax compliance. In essence, amortization spreads out expenses or costs systematically, whether in finance or accounting contexts.

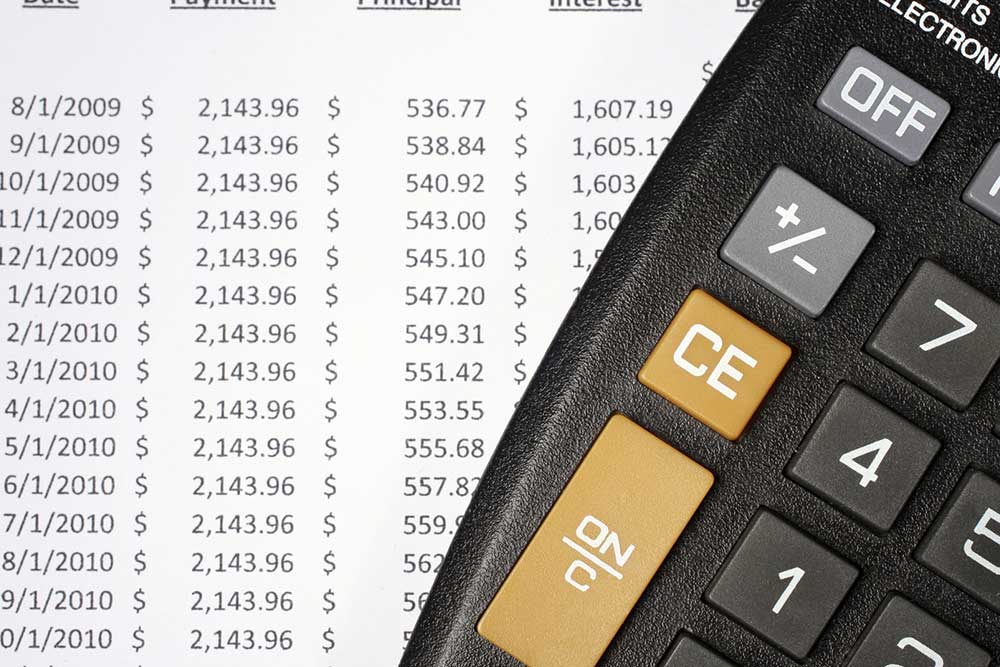

Creating an amortization schedule is crucial for understanding how each payment impacts your outstanding balance and the overall duration of your loan. Whether done manually, through online tools, or spreadsheet programs, generating this schedule helps borrowers visualize their repayment journey and plan accordingly.

The step-by-step process of creating an amortization schedule includes:

Identifying the initial loan amount — this is the principal borrowed from the lender.

Calculating the fixed monthly repayment — a consistent payment amount determined by loan terms.

Determining the interest portion of each payment — based on the prevailing interest rate applied to the remaining balance.

Subtracting the interest from the total payment to find out the principal repayment for that period.

Updating the remaining loan balance after each payment.

Repeating these steps monthly until the loan is fully paid off.

Loan amortization varies depending on the type of loan, each with its unique characteristics and repayment strategies:

Mortgage Loans

These are typically long-term loans spanning 15 to 30 years, often with fixed interest rates. Mortgages can be paid off early through refinancing, selling the property, or making additional payments. Consistent monthly payments help borrowers systematically reduce the principal while covering interest costs.

Personal Loans

Offered by banks, credit unions, or online lenders, personal loans are usually smaller in size and used for various needs such as debt consolidation, emergencies, or education. These loans generally have fixed terms of around three years, with stable interest rates, making repayment straightforward and predictable.

Auto Loans

Auto loans are designed specifically for vehicle financing. They tend to have shorter terms, usually between three to seven years. The amortization process involves fixed monthly payments that gradually reduce the principal, with interest calculated based on the remaining balance.

Understanding the nuances of loan amortization is essential for effective financial management. Compatibility with your financial goals, such as paying off a mortgage early or managing short-term borrowing costs, depends on choosing the right loan type and repayment strategy. Borrowers can use amortization schedules to plan extra payments, identify interest savings, and better understand how their payments influence the total interest paid over the life of the loan.